In 2030, all 70+ million baby boomers will have reached the age of 65 or older making them eligible to enroll in the medicare social health care system. With this date rapidly approaching it got us thinking about what exactly would happen to the current private health insurance system used by most employers to offer benefits to employees.

Here are some interesting 2019 stats from Census.gov:

• In 2019, 8.0 percent of people, or 26.1 million, did not have health insurance at any point during the year, according to the CPS ASEC. The percentage of people with health insurance coverage for all or part of 2019 was 92.0 percent.

• Private health insurance coverage was more prevalent than public coverage, covering 68.0 and 34.1 percent of the population at some point during the year, respectively. Employment-based insurance was the most common subtype.

• In 2019, 9.2 percent of people, or 29.6 million, were not covered by health insurance at the time of interview, according to the ACS, up from 8.9 percent and 28.6 million.

.• In 2019, the percentage of people with employer-provided coverage at the time of interview was slightly higher than in 2018, from 55.2 percent in 2018 to 55.4 percent in 2019.

• The percentage of people with Medicaid coverage at the time of interview decreased to 19.8 percent in 2019, down from 20.5 percent in 2018.

To summarize, 68% of Americans had private health insurance and 34% had public health insurance at some point and 8% had no coverage at all in 2019. With a current population of 330 million we can break this down the following:

Total population: 330 million – 8% uninsured = 303.6 million insured.

303.6 x 60% (private insurance) = 182 million

303.6 x 30% (public insurance) = 91 million

By 2030, we can expect 70 million boomers to enroll in medicare. The projected population of the United States is expected to be 360 million the same year. If we assume the rate of uninsured remains around 8 percent that would equate to about 28.8 million uninsured, 70 million enrolled in medicare would leave 260 million Americans to fend for themselves and if we assume that 30% will be on public assistance then that will leave 182 million looking for private insurance. The glaring problem however is that the top heavy 70 million boomers will consume far more health care than the younger populations but will have the taxpayer supporting them not private health insurance.

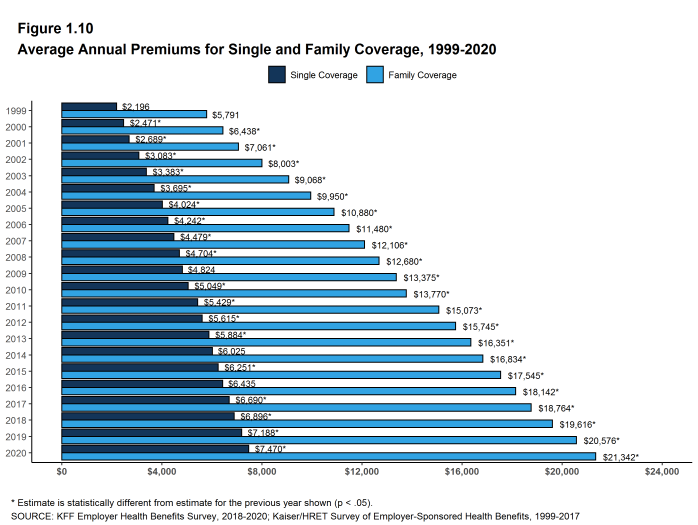

Using the data set from Kff.org, if we extrapolate the cost of insurance into 2030 using trends, “Single” coverage would cost $9500 per year in premiums and “Family” coverage would cost a whopping $28,000 per year!

It won’t only be insurance premiums that go up in cost however, the high demand for health care services from boomers will place huge demand on the health care system. Boomers will be competing with each other in far greater numbers than they do now.

The data from CMS.GOV provides a treasure trove of data and projections through 2028 and the data is surprising and depressing. Spending on Medicare is expected to hit $6.2 trillion in 2028. Here are some key forecast stats:

- National health spending is projected to grow at an average annual rate of 5.4 percent for 2019-28 and to reach $6.2 trillion by 2028.

- Because national health expenditures are projected to grow 1.1 percentage points faster than gross domestic product per year on average over 2019–28, the health share of the economy is projected to rise from 17.7 percent in 2018 to 19.7 percent in 2028.

- Price growth for medical goods and services (as measured by the personal health care deflator) is projected to accelerate, averaging 2.4 percent per year for 2019–28, partly reflecting faster expected growth in health sector wages.

- Among major payers, Medicare is expected to experience the fastest spending growth (7.6 percent per year over 2019-28), largely as a result of having the highest projected enrollment

- growth.

- The insured share of the population is expected to fall from 90.6 percent in 2018 to 89.4 percent by 2028.

There is lots of information to digest here but more importantly it provides a good basis to review our investment portfolio and act accordingly. Health care demand will go UP but the ability to pay for it will go DOWN. These healthcare service will also drain money away from other areas of the economy. As always, in any future event there will be winners and losers and it’s important to invest in the winners and not the losers.

Stay tuned!